| Multiple Linear Regression - Estimated Regression Equation |

| barrels_purchased[t] = + 2017.47 -370.92unit_price[t] + 338.291US_IND_PROD[t] -614.346dum[t] + 0.270976`barrels_purchased(t-1)`[t] + 0.234394`barrels_purchased(t-2)`[t] + 0.117325`barrels_purchased(t-3)`[t] + 0.307988`barrels_purchased(t-1s)`[t] + e[t] |

| Warning: you did not specify the column number of the endogenous series! The first column was selected by default. |

| Multiple Linear Regression - Ordinary Least Squares | |||||

| Variable | Parameter | S.D. | T-STAT H0: parameter = 0 | 2-tail p-value | 1-tail p-value |

| (Intercept) | +2018 | 6981 | +2.8900e-01 | 0.7727 | 0.3864 |

| unit_price | -370.9 | 97.38 | -3.8090e+00 | 0.0001616 | 8.082e-05 |

| US_IND_PROD | +338.3 | 161.7 | +2.0920e+00 | 0.03709 | 0.01854 |

| dum | -614.4 | 3475 | -1.7680e-01 | 0.8598 | 0.4299 |

| `barrels_purchased(t-1)` | +0.271 | 0.04773 | +5.6770e+00 | 2.652e-08 | 1.326e-08 |

| `barrels_purchased(t-2)` | +0.2344 | 0.04768 | +4.9160e+00 | 1.298e-06 | 6.488e-07 |

| `barrels_purchased(t-3)` | +0.1173 | 0.04639 | +2.5290e+00 | 0.01182 | 0.00591 |

| `barrels_purchased(t-1s)` | +0.308 | 0.03918 | +7.8600e+00 | 3.649e-14 | 1.824e-14 |

| Multiple Linear Regression - Regression Statistics | |

| Multiple R | 0.9668 |

| R-squared | 0.9348 |

| Adjusted R-squared | 0.9336 |

| F-TEST (value) | 812.7 |

| F-TEST (DF numerator) | 7 |

| F-TEST (DF denominator) | 397 |

| p-value | 0 |

| Multiple Linear Regression - Residual Statistics | |

| Residual Standard Deviation | 1.803e+04 |

| Sum Squared Residuals | 1.29e+11 |

| Menu of Residual Diagnostics | |

| Description | Link |

| Histogram | Compute |

| Central Tendency | Compute |

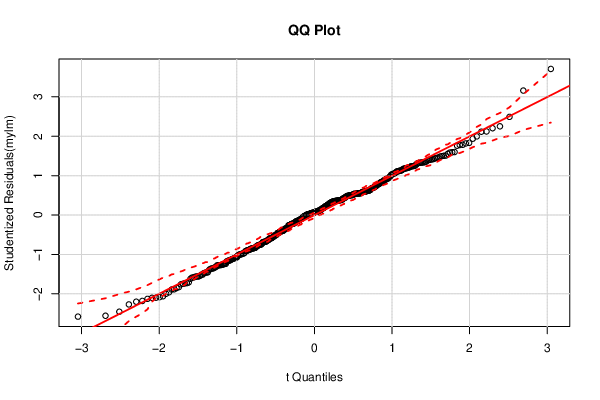

| QQ Plot | Compute |

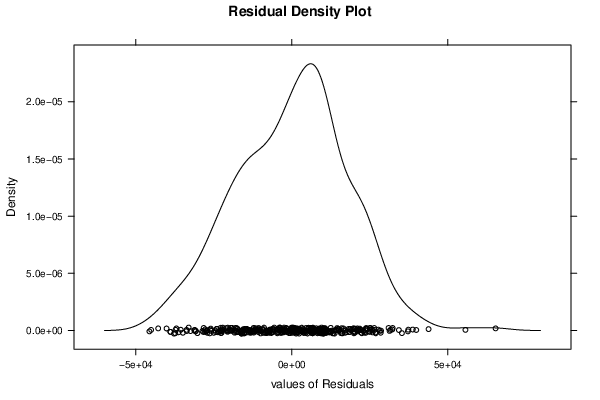

| Kernel Density Plot | Compute |

| Skewness/Kurtosis Test | Compute |

| Skewness-Kurtosis Plot | Compute |

| Harrell-Davis Plot | Compute |

| Bootstrap Plot -- Central Tendency | Compute |

| Blocked Bootstrap Plot -- Central Tendency | Compute |

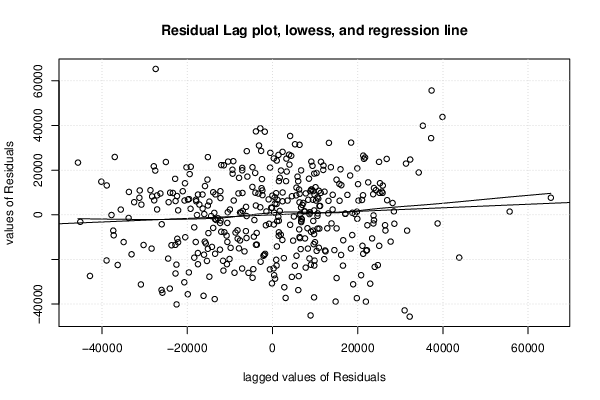

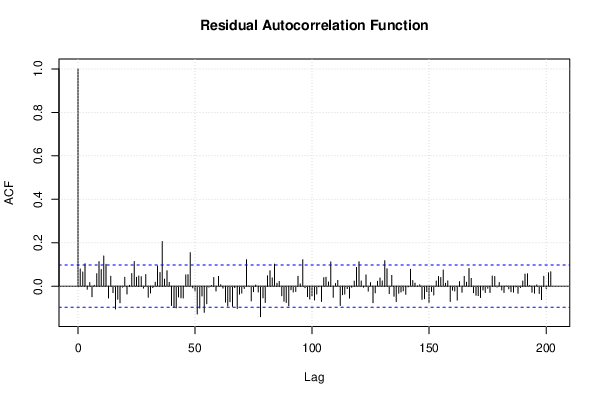

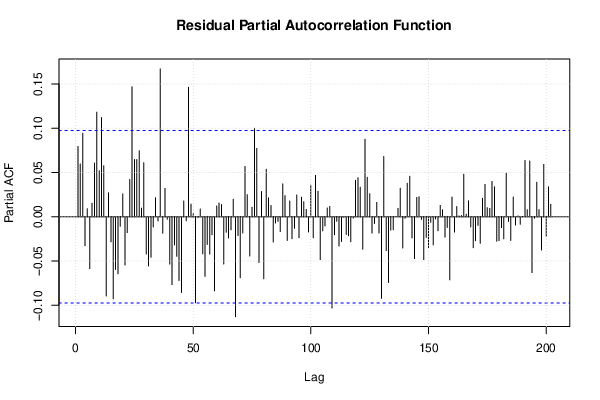

| (Partial) Autocorrelation Plot | Compute |

| Spectral Analysis | Compute |

| Tukey lambda PPCC Plot | Compute |

| Box-Cox Normality Plot | Compute |

| Summary Statistics | Compute |

| Ramsey RESET F-Test for powers (2 and 3) of fitted values |

> reset_test_fitted RESET test data: mylm RESET = 0.85408, df1 = 2, df2 = 395, p-value = 0.4265 |

| Ramsey RESET F-Test for powers (2 and 3) of regressors |

> reset_test_regressors RESET test data: mylm RESET = 2.1296, df1 = 14, df2 = 383, p-value = 0.009954 |

| Ramsey RESET F-Test for powers (2 and 3) of principal components |

> reset_test_principal_components RESET test data: mylm RESET = 1.7416, df1 = 2, df2 = 395, p-value = 0.1766 |

| Variance Inflation Factors (Multicollinearity) |

> vif

unit_price US_IND_PROD dum

1.981365 11.788899 3.460126

`barrels_purchased(t-1)` `barrels_purchased(t-2)` `barrels_purchased(t-3)`

13.906291 13.917632 13.176446

`barrels_purchased(t-1s)`

9.256817

|