| Multiple Linear Regression - Estimated Regression Equation |

| YY[t] = + 67.7757 + 7.70333X1[t] -11.1058X2[t] + 6.25483X3[t] + e[t] |

| Multiple Linear Regression - Ordinary Least Squares | |||||

| Variable | Parameter | S.D. | T-STAT H0: parameter = 0 | 2-tail p-value | 1-tail p-value |

| (Intercept) | +67.78 | 27.09 | +2.5020e+00 | 0.04088 | 0.02044 |

| X1 | +7.703 | 2.082 | +3.7010e+00 | 0.007649 | 0.003824 |

| X2 | -11.11 | 4.036 | -2.7520e+00 | 0.02844 | 0.01422 |

| X3 | +6.255 | 1.997 | +3.1320e+00 | 0.01657 | 0.008287 |

| Multiple Linear Regression - Regression Statistics | |

| Multiple R | 0.8294 |

| R-squared | 0.688 |

| Adjusted R-squared | 0.5542 |

| F-TEST (value) | 5.144 |

| F-TEST (DF numerator) | 3 |

| F-TEST (DF denominator) | 7 |

| p-value | 0.03436 |

| Multiple Linear Regression - Residual Statistics | |

| Residual Standard Deviation | 19.19 |

| Sum Squared Residuals | 2578 |

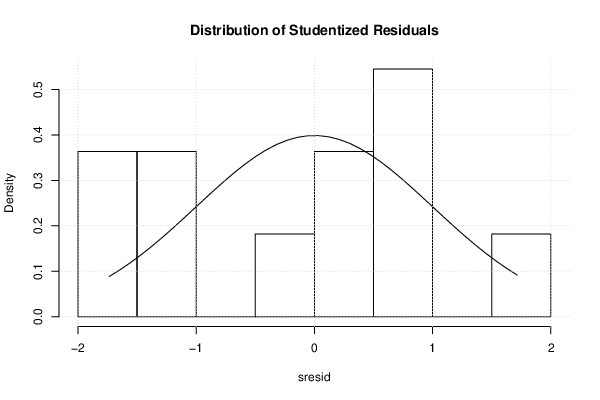

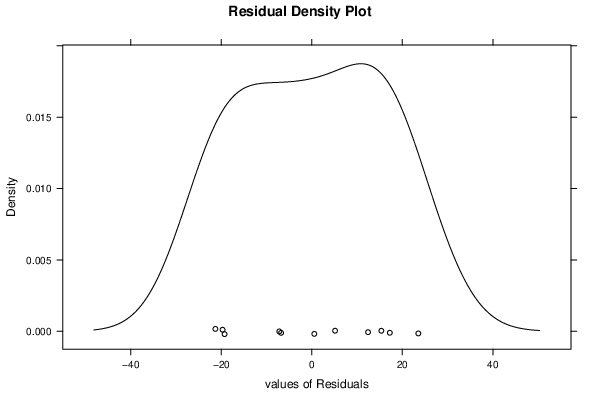

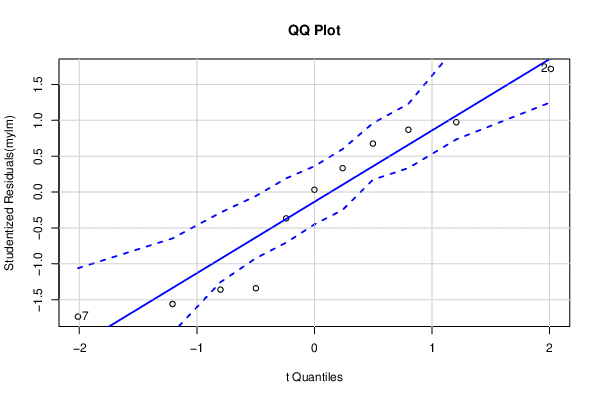

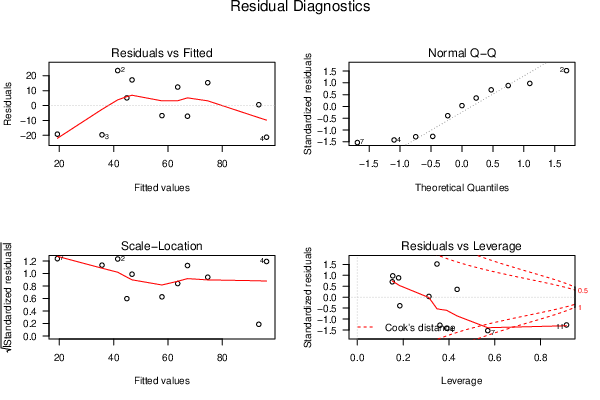

| Menu of Residual Diagnostics | |

| Description | Link |

| Histogram | Compute |

| Central Tendency | Compute |

| QQ Plot | Compute |

| Kernel Density Plot | Compute |

| Skewness/Kurtosis Test | Compute |

| Skewness-Kurtosis Plot | Compute |

| Harrell-Davis Plot | Compute |

| Bootstrap Plot -- Central Tendency | Compute |

| Blocked Bootstrap Plot -- Central Tendency | Compute |

| (Partial) Autocorrelation Plot | Compute |

| Spectral Analysis | Compute |

| Tukey lambda PPCC Plot | Compute |

| Box-Cox Normality Plot | Compute |

| Summary Statistics | Compute |

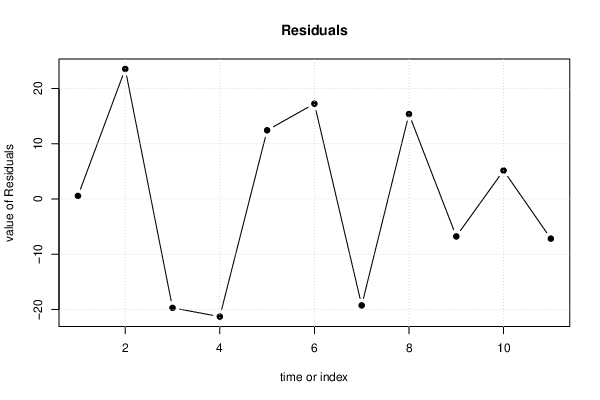

| Multiple Linear Regression - Actuals, Interpolation, and Residuals | |||

| Time or Index | Actuals | Interpolation Forecast | Residuals Prediction Error |

| 1 | 94 | 93.45 | 0.5527 |

| 2 | 65 | 41.48 | 23.52 |

| 3 | 16 | 35.71 | -19.71 |

| 4 | 75 | 96.3 | -21.3 |

| 5 | 76 | 63.58 | 12.42 |

| 6 | 64 | 46.77 | 17.23 |

| 7 | 0 | 19.27 | -19.27 |

| 8 | 90 | 74.64 | 15.36 |

| 9 | 51 | 57.78 | -6.783 |

| 10 | 50 | 44.86 | 5.143 |

| 11 | 60 | 67.18 | -7.181 |

| Ramsey RESET F-Test for powers (2 and 3) of fitted values |

> reset_test_fitted RESET test data: mylm RESET = 2.1554, df1 = 2, df2 = 5, p-value = 0.2113 |

| Ramsey RESET F-Test for powers (2 and 3) of regressors |

> reset_test_regressors RESET test data: mylm RESET = 1.1201, df1 = 6, df2 = 1, p-value = 0.6188 |

| Ramsey RESET F-Test for powers (2 and 3) of principal components |

> reset_test_principal_components RESET test data: mylm RESET = 0.088001, df1 = 2, df2 = 5, p-value = 0.9171 |

| Variance Inflation Factors (Multicollinearity) |

> vif

X1 X2 X3

1.846086 1.841739 1.587416

|