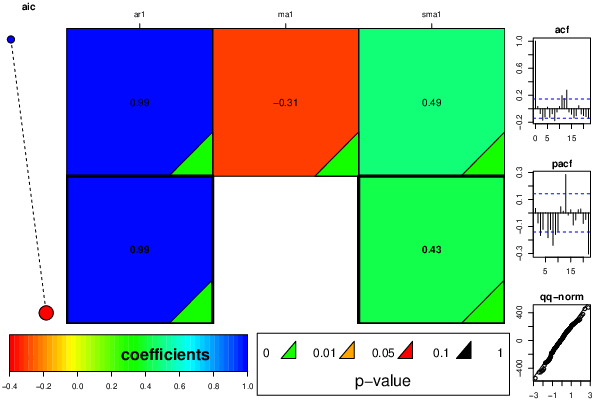

| ARIMA Parameter Estimation and Backward Selection | |||

| Iteration | ar1 | ma1 | sma1 |

| Estimates ( 1 ) | 0.9939 | -0.314 | 0.491 |

| (p-val) | (0 ) | (0.0012 ) | (0 ) |

| Estimates ( 2 ) | 0.9873 | 0 | 0.4267 |

| (p-val) | (0 ) | (NA ) | (0 ) |

| Estimates ( 3 ) | NA | NA | NA |

| (p-val) | (NA ) | (NA ) | (NA ) |

| Estimates ( 4 ) | NA | NA | NA |

| (p-val) | (NA ) | (NA ) | (NA ) |

| Estimates ( 5 ) | NA | NA | NA |

| (p-val) | (NA ) | (NA ) | (NA ) |

| Menu of Residual Diagnostics | |

| Description | Link |

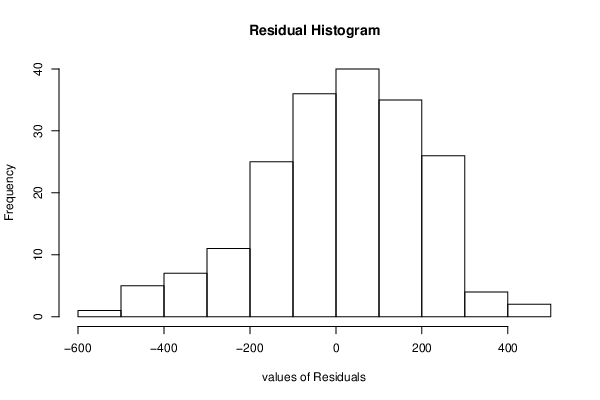

| Histogram | Compute |

| Central Tendency | Compute |

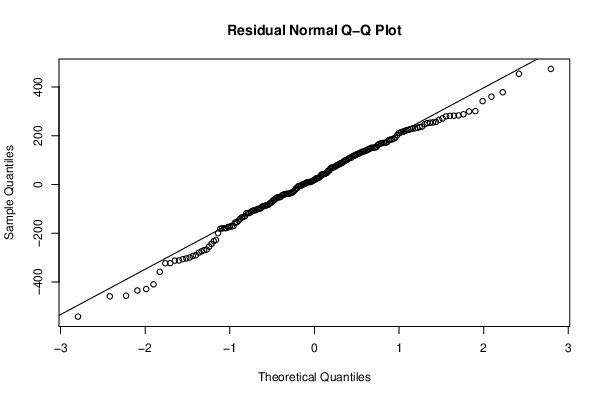

| QQ Plot | Compute |

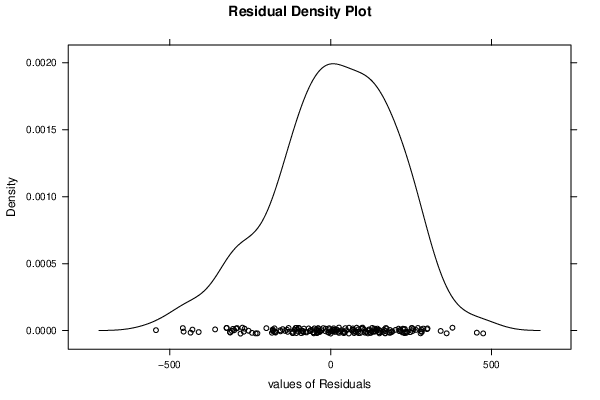

| Kernel Density Plot | Compute |

| Skewness/Kurtosis Test | Compute |

| Skewness-Kurtosis Plot | Compute |

| Harrell-Davis Plot | Compute |

| Bootstrap Plot -- Central Tendency | Compute |

| Blocked Bootstrap Plot -- Central Tendency | Compute |

| (Partial) Autocorrelation Plot | Compute |

| Spectral Analysis | Compute |

| Tukey lambda PPCC Plot | Compute |

| Box-Cox Normality Plot | Compute |

| Summary Statistics | Compute |