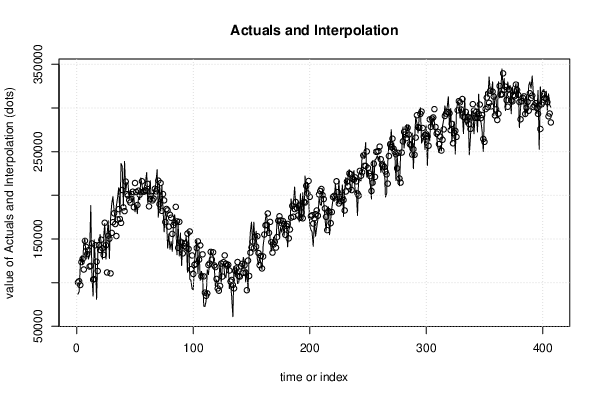

| Multiple Linear Regression - Estimated Regression Equation |

| barrels_purchased[t] = + 7323.02 -381.068unit_price[t] + 108.332cpi[t] + 0.528378`barrels_purchased(t-1)`[t] + 0.424374`barrels_purchased(t-1s)`[t] + e[t] |

| Multiple Linear Regression - Ordinary Least Squares | |||||

| Variable | Parameter | S.D. | T-STAT H0: parameter = 0 | 2-tail p-value | 1-tail p-value |

| (Intercept) | +7323 | 3140 | +2.3320e+00 | 0.0202 | 0.0101 |

| unit_price | -381.1 | 88.32 | -4.3150e+00 | 2.014e-05 | 1.007e-05 |

| cpi | +108.3 | 36.9 | +2.9360e+00 | 0.003519 | 0.00176 |

| `barrels_purchased(t-1)` | +0.5284 | 0.03731 | +1.4160e+01 | 3.248e-37 | 1.624e-37 |

| `barrels_purchased(t-1s)` | +0.4244 | 0.03832 | +1.1070e+01 | 4.679e-25 | 2.339e-25 |

| Multiple Linear Regression - Regression Statistics | |

| Multiple R | 0.9619 |

| R-squared | 0.9252 |

| Adjusted R-squared | 0.9245 |

| F-TEST (value) | 1243 |

| F-TEST (DF numerator) | 4 |

| F-TEST (DF denominator) | 402 |

| p-value | 0 |

| Multiple Linear Regression - Residual Statistics | |

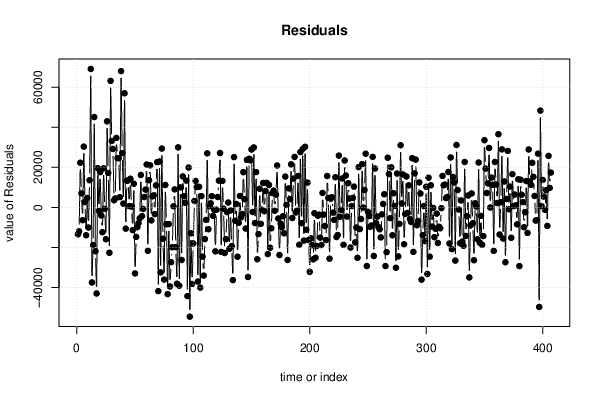

| Residual Standard Deviation | 1.932e+04 |

| Sum Squared Residuals | 1.501e+11 |

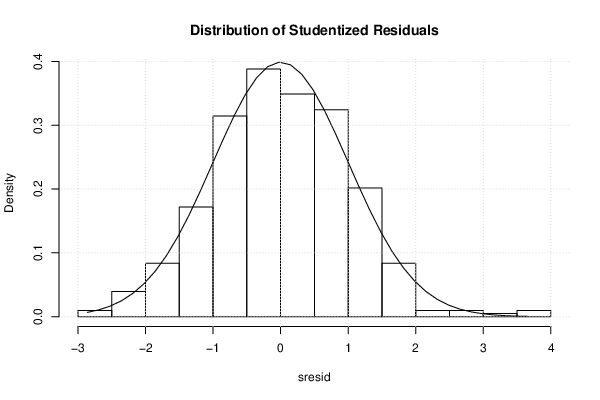

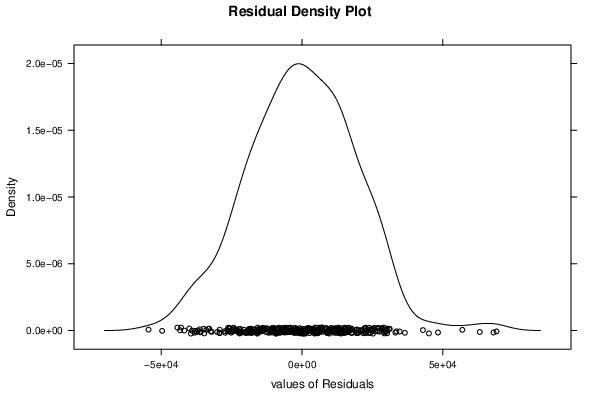

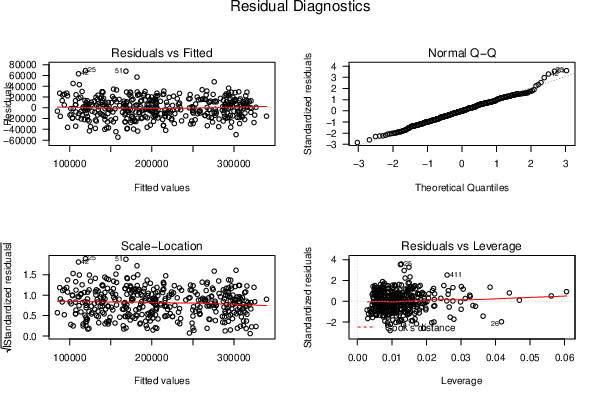

| Menu of Residual Diagnostics | |

| Description | Link |

| Histogram | Compute |

| Central Tendency | Compute |

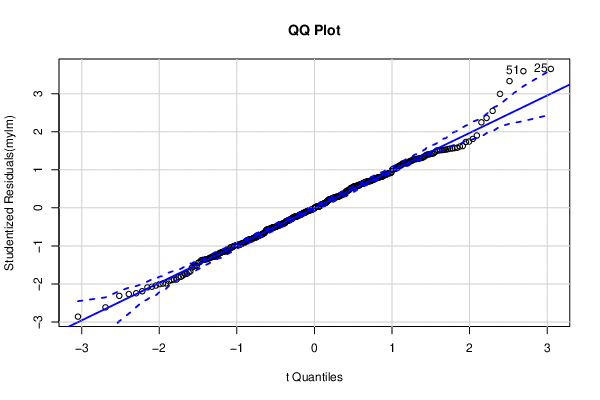

| QQ Plot | Compute |

| Kernel Density Plot | Compute |

| Skewness/Kurtosis Test | Compute |

| Skewness-Kurtosis Plot | Compute |

| Harrell-Davis Plot | Compute |

| Bootstrap Plot -- Central Tendency | Compute |

| Blocked Bootstrap Plot -- Central Tendency | Compute |

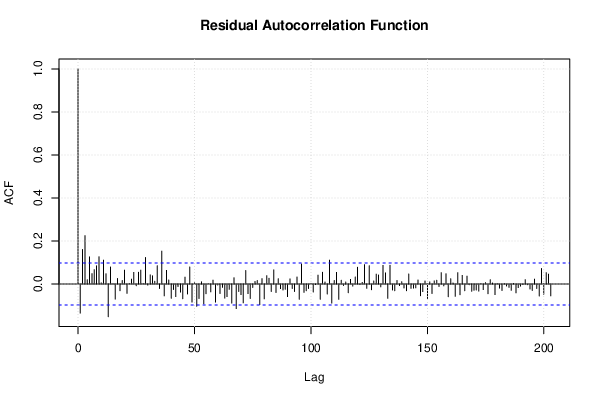

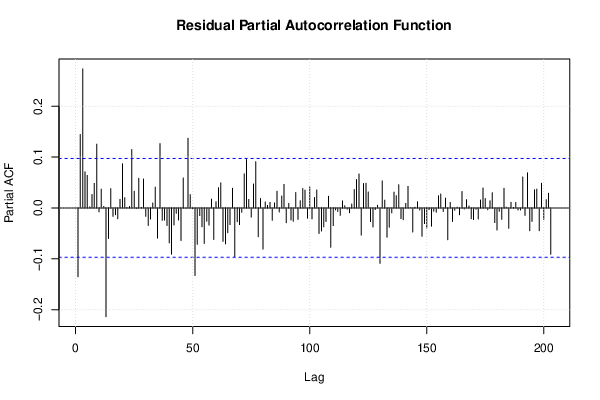

| (Partial) Autocorrelation Plot | Compute |

| Spectral Analysis | Compute |

| Tukey lambda PPCC Plot | Compute |

| Box-Cox Normality Plot | Compute |

| Summary Statistics | Compute |

| Ramsey RESET F-Test for powers (2 and 3) of fitted values |

> reset_test_fitted RESET test data: mylm RESET = 1.7122, df1 = 2, df2 = 400, p-value = 0.1818 |

| Ramsey RESET F-Test for powers (2 and 3) of regressors |

> reset_test_regressors RESET test data: mylm RESET = 7.8458, df1 = 8, df2 = 394, p-value = 8.46e-10 |

| Ramsey RESET F-Test for powers (2 and 3) of principal components |

> reset_test_principal_components RESET test data: mylm RESET = 2.846, df1 = 2, df2 = 400, p-value = 0.05925 |

| Variance Inflation Factors (Multicollinearity) |

> vif

unit_price cpi `barrels_purchased(t-1)`

1.426005 3.101454 7.498729

`barrels_purchased(t-1s)`

7.785503

|