| Multiple Linear Regression - Estimated Regression Equation |

| SP[t] = -250.155 + 73.3043V[t] -0.171478SQ[t] + 27.6031BR[t] -78.6611PH[t] + 50.6011GR[t] -6.22991PK[t] + 8.44973AG[t] + 82.5753Re[t] + 1.15958As[t] + 137.4C[t] -25.7549TH[t] + e[t] |

| Multiple Linear Regression - Ordinary Least Squares | |||||

| Variable | Parameter | S.D. | T-STAT H0: parameter = 0 | 2-tail p-value | 1-tail p-value |

| (Intercept) | -250.2 | 103.1 | -2.4270e+00 | 0.02597 | 0.01298 |

| V | +73.3 | 49.59 | +1.4780e+00 | 0.1567 | 0.07834 |

| SQ | -0.1715 | 0.09469 | -1.8110e+00 | 0.08687 | 0.04343 |

| BR | +27.6 | 45.97 | +6.0050e-01 | 0.5556 | 0.2778 |

| PH | -78.66 | 47.75 | -1.6470e+00 | 0.1168 | 0.05842 |

| GR | +50.6 | 50.83 | +9.9540e-01 | 0.3327 | 0.1664 |

| PK | -6.23 | 46.29 | -1.3460e-01 | 0.8944 | 0.4472 |

| AG | +8.45 | 3.18 | +2.6570e+00 | 0.01605 | 0.008023 |

| Re | +82.58 | 48.56 | +1.7010e+00 | 0.1062 | 0.05312 |

| As | +1.16 | 0.1378 | +8.4140e+00 | 1.185e-07 | 5.925e-08 |

| C | +137.4 | 42.22 | +3.2540e+00 | 0.004405 | 0.002202 |

| TH | -25.75 | 70.41 | -3.6580e-01 | 0.7188 | 0.3594 |

| Multiple Linear Regression - Regression Statistics | |

| Multiple R | 0.9833 |

| R-squared | 0.9669 |

| Adjusted R-squared | 0.9467 |

| F-TEST (value) | 47.86 |

| F-TEST (DF numerator) | 11 |

| F-TEST (DF denominator) | 18 |

| p-value | 5.011e-11 |

| Multiple Linear Regression - Residual Statistics | |

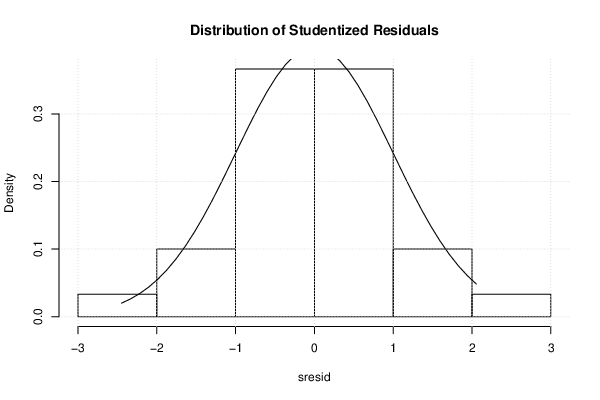

| Residual Standard Deviation | 77.03 |

| Sum Squared Residuals | 1.068e+05 |

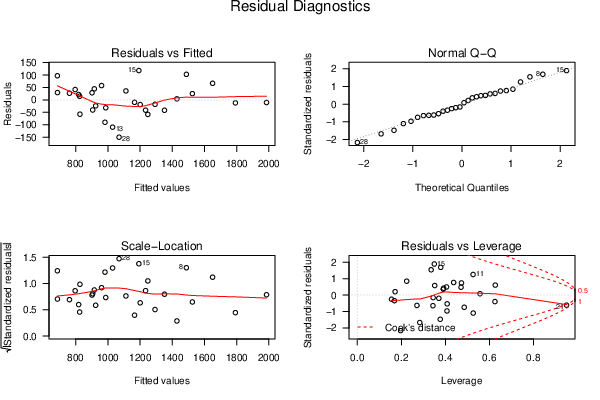

| Menu of Residual Diagnostics | |

| Description | Link |

| Histogram | Compute |

| Central Tendency | Compute |

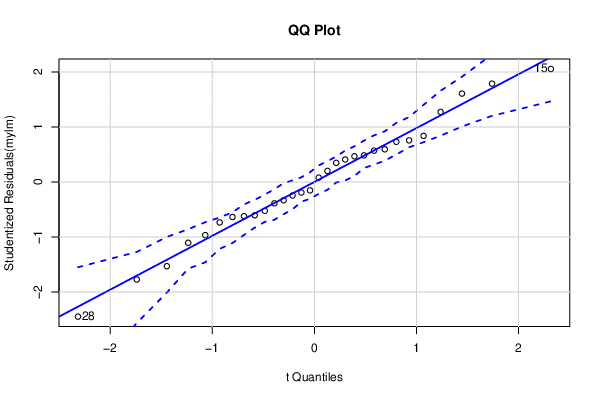

| QQ Plot | Compute |

| Kernel Density Plot | Compute |

| Skewness/Kurtosis Test | Compute |

| Skewness-Kurtosis Plot | Compute |

| Harrell-Davis Plot | Compute |

| Bootstrap Plot -- Central Tendency | Compute |

| Blocked Bootstrap Plot -- Central Tendency | Compute |

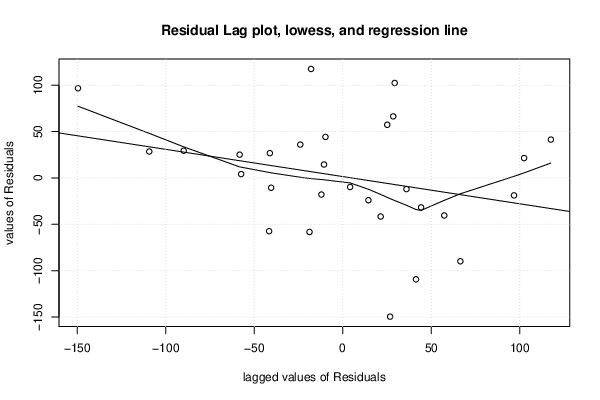

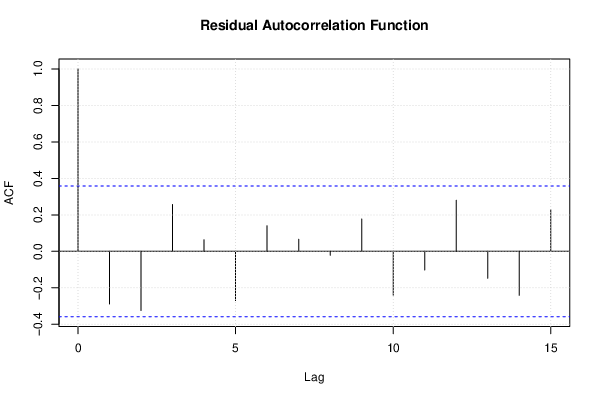

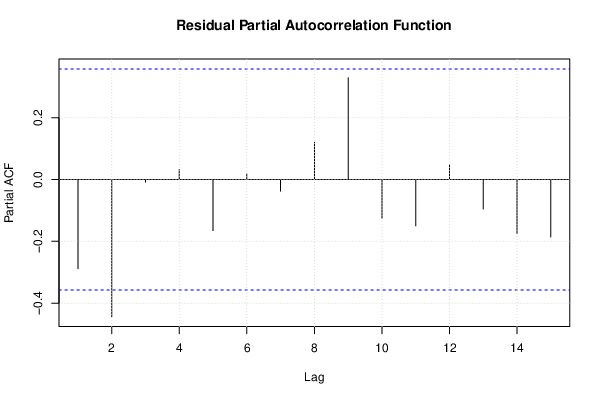

| (Partial) Autocorrelation Plot | Compute |

| Spectral Analysis | Compute |

| Tukey lambda PPCC Plot | Compute |

| Box-Cox Normality Plot | Compute |

| Summary Statistics | Compute |

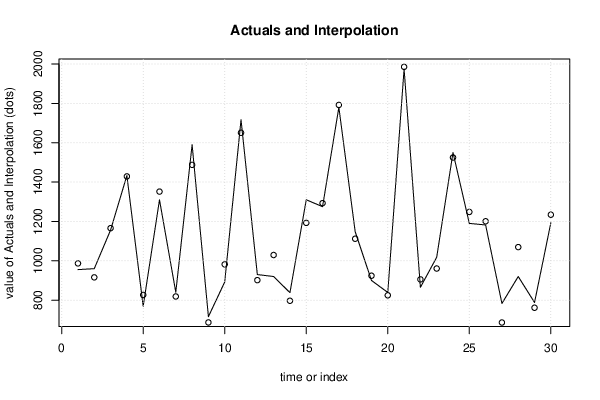

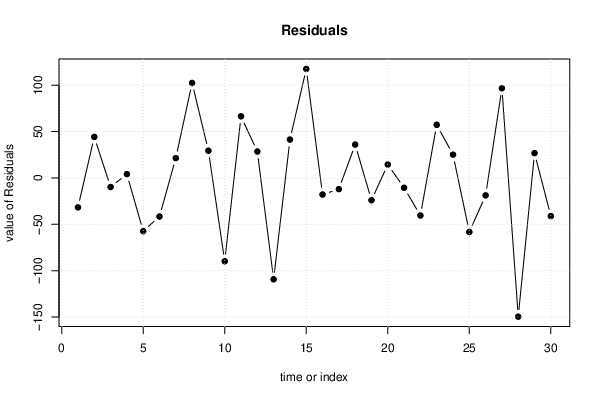

| Multiple Linear Regression - Actuals, Interpolation, and Residuals | |||

| Time or Index | Actuals | Interpolation Forecast | Residuals Prediction Error |

| 1 | 955 | 986.7 | -31.73 |

| 2 | 960 | 915.7 | 44.27 |

| 3 | 1156 | 1166 | -9.75 |

| 4 | 1433 | 1429 | 4.177 |

| 5 | 769 | 826.4 | -57.38 |

| 6 | 1310 | 1352 | -41.58 |

| 7 | 840 | 818.5 | 21.45 |

| 8 | 1590 | 1488 | 102.4 |

| 9 | 716 | 686.6 | 29.36 |

| 10 | 892 | 981.8 | -89.84 |

| 11 | 1717 | 1651 | 66.46 |

| 12 | 930 | 901.5 | 28.52 |

| 13 | 920 | 1029 | -109.3 |

| 14 | 838 | 796.6 | 41.39 |

| 15 | 1310 | 1192 | 117.6 |

| 16 | 1275 | 1293 | -17.88 |

| 17 | 1780 | 1792 | -12.03 |

| 18 | 1148 | 1112 | 36.01 |

| 19 | 900 | 924 | -23.98 |

| 20 | 839 | 824.5 | 14.5 |

| 21 | 1975 | 1986 | -10.56 |

| 22 | 865 | 905.4 | -40.42 |

| 23 | 1018 | 960.7 | 57.35 |

| 24 | 1550 | 1525 | 25.15 |

| 25 | 1190 | 1248 | -58.24 |

| 26 | 1182 | 1201 | -18.76 |

| 27 | 783 | 686.2 | 96.77 |

| 28 | 920 | 1070 | -149.6 |

| 29 | 788 | 761.2 | 26.76 |

| 30 | 1193 | 1234 | -41.16 |

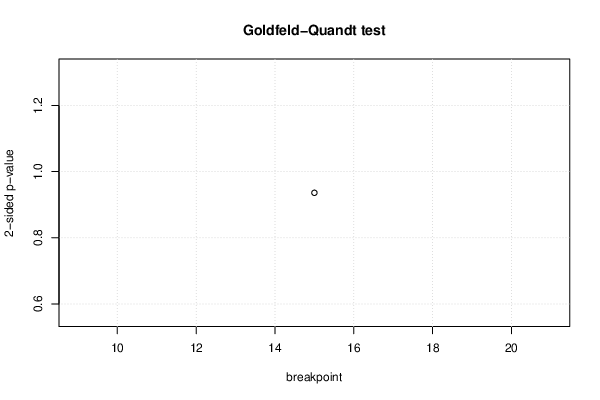

| Goldfeld-Quandt test for Heteroskedasticity | |||

| p-values | Alternative Hypothesis | ||

| breakpoint index | greater | 2-sided | less |

| 15 | 0.4679 | 0.9359 | 0.5321 |

| Meta Analysis of Goldfeld-Quandt test for Heteroskedasticity | |||

| Description | # significant tests | % significant tests | OK/NOK |

| 1% type I error level | 0 | 0 | OK |

| 5% type I error level | 0 | 0 | OK |

| 10% type I error level | 0 | 0 | OK |

| Ramsey RESET F-Test for powers (2 and 3) of fitted values |

> reset_test_fitted RESET test data: mylm RESET = 7.285, df1 = 2, df2 = 16, p-value = 0.005631 |

| Ramsey RESET F-Test for powers (2 and 3) of regressors |

> reset_test_regressors RESET test data: mylm RESET = -0.36952, df1 = 22, df2 = -4, p-value = NA |

| Ramsey RESET F-Test for powers (2 and 3) of principal components |

> reset_test_principal_components RESET test data: mylm RESET = 0.3125, df1 = 2, df2 = 16, p-value = 0.736 |

| Variance Inflation Factors (Multicollinearity) |

> vif

V SQ BR PH GR PK AG Re

1.639363 17.057586 3.335171 1.601112 1.509764 2.696835 3.891731 2.400751

As C TH

10.963412 2.243383 2.896230

|