par1 <- as.numeric(par1)

if (par2 == 'Single') K <- 1

if (par2 == 'Double') K <- 2

if (par2 == 'Triple') K <- par1

nx <- length(x)

nxmK <- nx - K

x <- ts(x, frequency = par1)

if (par2 == 'Single') fit <- HoltWinters(x, gamma=0, beta=0)

if (par2 == 'Double') fit <- HoltWinters(x, gamma=0)

if (par2 == 'Triple') fit <- HoltWinters(x, seasonal=par3)

fit

myresid <- x - fit$fitted[,'xhat']

bitmap(file='test1.png')

op <- par(mfrow=c(2,1))

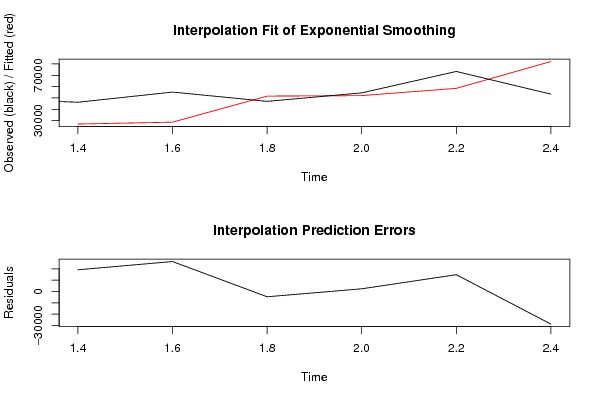

plot(fit,ylab='Observed (black) / Fitted (red)',main='Interpolation Fit of Exponential Smoothing')

plot(myresid,ylab='Residuals',main='Interpolation Prediction Errors')

par(op)

dev.off()

bitmap(file='test2.png')

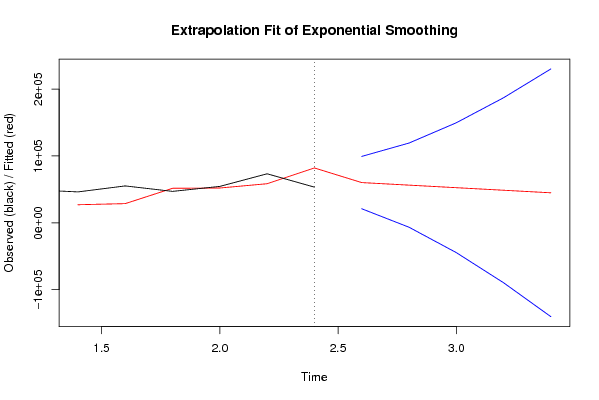

p <- predict(fit, par1, prediction.interval=TRUE)

np <- length(p[,1])

plot(fit,p,ylab='Observed (black) / Fitted (red)',main='Extrapolation Fit of Exponential Smoothing')

dev.off()

bitmap(file='test3.png')

op <- par(mfrow = c(2,2))

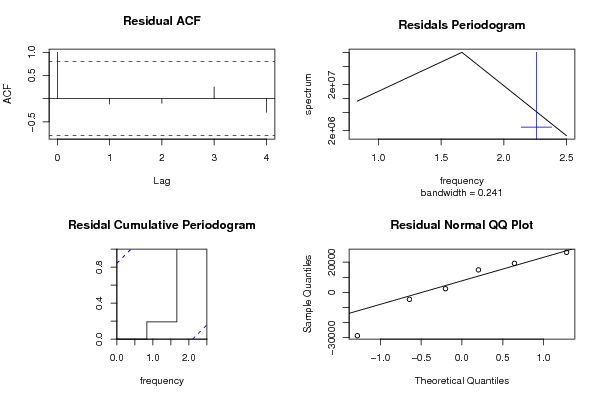

acf(as.numeric(myresid),lag.max = nx/2,main='Residual ACF')

spectrum(myresid,main='Residals Periodogram')

cpgram(myresid,main='Residal Cumulative Periodogram')

qqnorm(myresid,main='Residual Normal QQ Plot')

qqline(myresid)

par(op)

dev.off()

load(file='createtable')

a<-table.start()

a<-table.row.start(a)

a<-table.element(a,'Estimated Parameters of Exponential Smoothing',2,TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'Parameter',header=TRUE)

a<-table.element(a,'Value',header=TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'alpha',header=TRUE)

a<-table.element(a,fit$alpha)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'beta',header=TRUE)

a<-table.element(a,fit$beta)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'gamma',header=TRUE)

a<-table.element(a,fit$gamma)

a<-table.row.end(a)

a<-table.end(a)

table.save(a,file='mytable.tab')

a<-table.start()

a<-table.row.start(a)

a<-table.element(a,'Interpolation Forecasts of Exponential Smoothing',4,TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'t',header=TRUE)

a<-table.element(a,'Observed',header=TRUE)

a<-table.element(a,'Fitted',header=TRUE)

a<-table.element(a,'Residuals',header=TRUE)

a<-table.row.end(a)

for (i in 1:nxmK) {

a<-table.row.start(a)

a<-table.element(a,i+K,header=TRUE)

a<-table.element(a,x[i+K])

a<-table.element(a,fit$fitted[i,'xhat'])

a<-table.element(a,myresid[i])

a<-table.row.end(a)

}

a<-table.end(a)

table.save(a,file='mytable1.tab')

a<-table.start()

a<-table.row.start(a)

a<-table.element(a,'Extrapolation Forecasts of Exponential Smoothing',4,TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'t',header=TRUE)

a<-table.element(a,'Forecast',header=TRUE)

a<-table.element(a,'95% Lower Bound',header=TRUE)

a<-table.element(a,'95% Upper Bound',header=TRUE)

a<-table.row.end(a)

for (i in 1:np) {

a<-table.row.start(a)

a<-table.element(a,nx+i,header=TRUE)

a<-table.element(a,p[i,'fit'])

a<-table.element(a,p[i,'lwr'])

a<-table.element(a,p[i,'upr'])

a<-table.row.end(a)

}

a<-table.end(a)

table.save(a,file='mytable2.tab')

|