panel.tau <- function(x, y, digits=2, prefix='', cex.cor)

{

usr <- par('usr'); on.exit(par(usr))

par(usr = c(0, 1, 0, 1))

rr <- cor.test(x, y, method='kendall')

r <- round(rr$p.value,2)

txt <- format(c(r, 0.123456789), digits=digits)[1]

txt <- paste(prefix, txt, sep='')

if(missing(cex.cor)) cex <- 0.5/strwidth(txt)

text(0.5, 0.5, txt, cex = cex)

}

panel.hist <- function(x, ...)

{

usr <- par('usr'); on.exit(par(usr))

par(usr = c(usr[1:2], 0, 1.5) )

h <- hist(x, plot = FALSE)

breaks <- h$breaks; nB <- length(breaks)

y <- h$counts; y <- y/max(y)

rect(breaks[-nB], 0, breaks[-1], y, col='grey', ...)

}

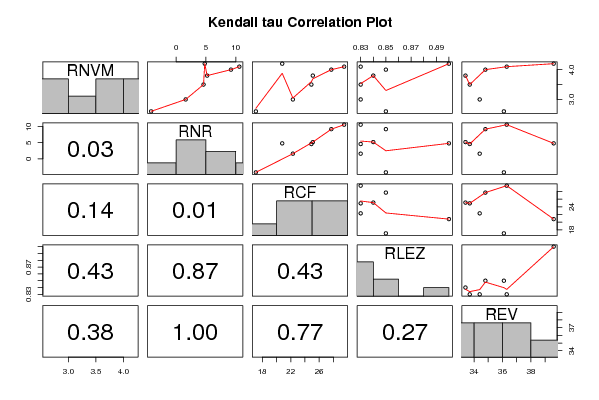

bitmap(file='test1.png')

pairs(t(y),diag.panel=panel.hist, upper.panel=panel.smooth, lower.panel=panel.tau, main=main)

dev.off()

load(file='createtable')

a<-table.start()

a<-table.row.start(a)

a<-table.element(a,'Kendall tau rank correlations for all pairs of data series',3,TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'pair',1,TRUE)

a<-table.element(a,'tau',1,TRUE)

a<-table.element(a,'p-value',1,TRUE)

a<-table.row.end(a)

n <- length(y[,1])

n

cor.test(y[1,],y[2,],method='kendall')

for (i in 1:(n-1))

{

for (j in (i+1):n)

{

a<-table.row.start(a)

dum <- paste('tau(',dimnames(t(x))[[2]][i])

dum <- paste(dum,',')

dum <- paste(dum,dimnames(t(x))[[2]][j])

dum <- paste(dum,')')

a<-table.element(a,dum,header=TRUE)

r <- cor.test(y[i,],y[j,],method='kendall')

a<-table.element(a,r$estimate)

a<-table.element(a,r$p.value)

a<-table.row.end(a)

}

}

a<-table.end(a)

table.save(a,file='mytable.tab')

|