library(lattice)

if (par1 == 'TRUE') par1 <- TRUE

if (par1 == 'FALSE') par1 <- FALSE

par2 <- as.numeric(par2) #Box-Cox lambda transformation parameter

par3 <- as.numeric(par3) #degree of non-seasonal differencing

par4 <- as.numeric(par4) #degree of seasonal differencing

par5 <- as.numeric(par5) #seasonal period

par6 <- as.numeric(par6) #degree (p) of the non-seasonal AR(p) polynomial

par7 <- as.numeric(par7) #degree (q) of the non-seasonal MA(q) polynomial

par8 <- as.numeric(par8) #degree (P) of the seasonal AR(P) polynomial

par9 <- as.numeric(par9) #degree (Q) of the seasonal MA(Q) polynomial

armaGR <- function(arima.out, names, n){

try1 <- arima.out$coef

try2 <- sqrt(diag(arima.out$var.coef))

try.data.frame <- data.frame(matrix(NA,ncol=4,nrow=length(names)))

dimnames(try.data.frame) <- list(names,c('coef','std','tstat','pv'))

try.data.frame[,1] <- try1

for(i in 1:length(try2)) try.data.frame[which(rownames(try.data.frame)==names(try2)[i]),2] <- try2[i]

try.data.frame[,3] <- try.data.frame[,1] / try.data.frame[,2]

try.data.frame[,4] <- round((1-pt(abs(try.data.frame[,3]),df=n-(length(try2)+1)))*2,5)

vector <- rep(NA,length(names))

vector[is.na(try.data.frame[,4])] <- 0

maxi <- which.max(try.data.frame[,4])

continue <- max(try.data.frame[,4],na.rm=TRUE) > .05

vector[maxi] <- 0

list(summary=try.data.frame,next.vector=vector,continue=continue)

}

arimaSelect <- function(series, order=c(13,0,0), seasonal=list(order=c(2,0,0),period=12), include.mean=F){

nrc <- order[1]+order[3]+seasonal$order[1]+seasonal$order[3]

coeff <- matrix(NA, nrow=nrc*2, ncol=nrc)

pval <- matrix(NA, nrow=nrc*2, ncol=nrc)

mylist <- rep(list(NULL), nrc)

names <- NULL

if(order[1] > 0) names <- paste('ar',1:order[1],sep='')

if(order[3] > 0) names <- c( names , paste('ma',1:order[3],sep='') )

if(seasonal$order[1] > 0) names <- c(names, paste('sar',1:seasonal$order[1],sep=''))

if(seasonal$order[3] > 0) names <- c(names, paste('sma',1:seasonal$order[3],sep=''))

arima.out <- arima(series, order=order, seasonal=seasonal, include.mean=include.mean, method='ML')

mylist[[1]] <- arima.out

last.arma <- armaGR(arima.out, names, length(series))

mystop <- FALSE

i <- 1

coeff[i,] <- last.arma[[1]][,1]

pval [i,] <- last.arma[[1]][,4]

i <- 2

aic <- arima.out$aic

while(!mystop){

mylist[[i]] <- arima.out

arima.out <- arima(series, order=order, seasonal=seasonal, include.mean=include.mean, method='ML', fixed=last.arma$next.vector)

aic <- c(aic, arima.out$aic)

last.arma <- armaGR(arima.out, names, length(series))

mystop <- !last.arma$continue

coeff[i,] <- last.arma[[1]][,1]

pval [i,] <- last.arma[[1]][,4]

i <- i+1

}

list(coeff, pval, mylist, aic=aic)

}

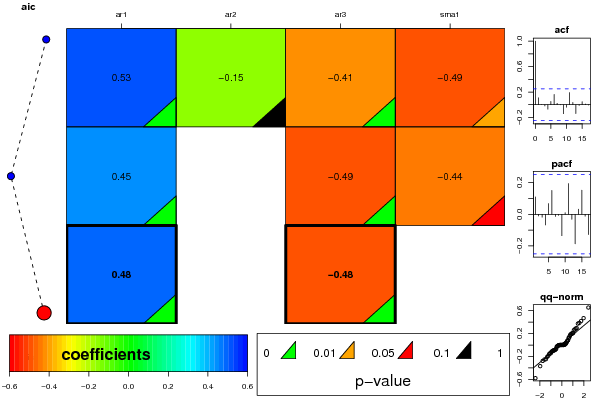

arimaSelectplot <- function(arimaSelect.out,noms,choix){

noms <- names(arimaSelect.out[[3]][[1]]$coef)

coeff <- arimaSelect.out[[1]]

k <- min(which(is.na(coeff[,1])))-1

coeff <- coeff[1:k,]

pval <- arimaSelect.out[[2]][1:k,]

aic <- arimaSelect.out$aic[1:k]

coeff[coeff==0] <- NA

n <- ncol(coeff)

if(missing(choix)) choix <- k

layout(matrix(c(1,1,1,2,

3,3,3,2,

3,3,3,4,

5,6,7,7),nr=4),

widths=c(10,35,45,15),

heights=c(30,30,15,15))

couleurs <- rainbow(75)[1:50]#(50)

ticks <- pretty(coeff)

par(mar=c(1,1,3,1))

plot(aic,k:1-.5,type='o',pch=21,bg='blue',cex=2,axes=F,lty=2,xpd=NA)

points(aic[choix],k-choix+.5,pch=21,cex=4,bg=2,xpd=NA)

title('aic',line=2)

par(mar=c(3,0,0,0))

plot(0,axes=F,xlab='',ylab='',xlim=range(ticks),ylim=c(.1,1))

rect(xleft = min(ticks) + (0:49)/50*(max(ticks)-min(ticks)),

xright = min(ticks) + (1:50)/50*(max(ticks)-min(ticks)),

ytop = rep(1,50),

ybottom= rep(0,50),col=couleurs,border=NA)

axis(1,ticks)

rect(xleft=min(ticks),xright=max(ticks),ytop=1,ybottom=0)

text(mean(coeff,na.rm=T),.5,'coefficients',cex=2,font=2)

par(mar=c(1,1,3,1))

image(1:n,1:k,t(coeff[k:1,]),axes=F,col=couleurs,zlim=range(ticks))

for(i in 1:n) for(j in 1:k) if(!is.na(coeff[j,i])) {

if(pval[j,i]<.01) symb = 'green'

else if( (pval[j,i]<.05) & (pval[j,i]>=.01)) symb = 'orange'

else if( (pval[j,i]<.1) & (pval[j,i]>=.05)) symb = 'red'

else symb = 'black'

polygon(c(i+.5 ,i+.2 ,i+.5 ,i+.5),

c(k-j+0.5,k-j+0.5,k-j+0.8,k-j+0.5),

col=symb)

if(j==choix) {

rect(xleft=i-.5,

xright=i+.5,

ybottom=k-j+1.5,

ytop=k-j+.5,

lwd=4)

text(i,

k-j+1,

round(coeff[j,i],2),

cex=1.2,

font=2)

}

else{

rect(xleft=i-.5,xright=i+.5,ybottom=k-j+1.5,ytop=k-j+.5)

text(i,k-j+1,round(coeff[j,i],2),cex=1.2,font=1)

}

}

axis(3,1:n,noms)

par(mar=c(0.5,0,0,0.5))

plot(0,axes=F,xlab='',ylab='',type='n',xlim=c(0,8),ylim=c(-.2,.8))

cols <- c('green','orange','red','black')

niv <- c('0','0.01','0.05','0.1')

for(i in 0:3){

polygon(c(1+2*i ,1+2*i ,1+2*i-.5 ,1+2*i),

c(.4 ,.7 , .4 , .4),

col=cols[i+1])

text(2*i,0.5,niv[i+1],cex=1.5)

}

text(8,.5,1,cex=1.5)

text(4,0,'p-value',cex=2)

box()

residus <- arimaSelect.out[[3]][[choix]]$res

par(mar=c(1,2,4,1))

acf(residus,main='')

title('acf',line=.5)

par(mar=c(1,2,4,1))

pacf(residus,main='')

title('pacf',line=.5)

par(mar=c(2,2,4,1))

qqnorm(residus,main='')

title('qq-norm',line=.5)

qqline(residus)

residus

}

if (par2 == 0) x <- log(x)

if (par2 != 0) x <- x^par2

(selection <- arimaSelect(x, order=c(par6,par3,par7), seasonal=list(order=c(par8,par4,par9), period=par5)))

bitmap(file='test1.png')

resid <- arimaSelectplot(selection)

dev.off()

resid

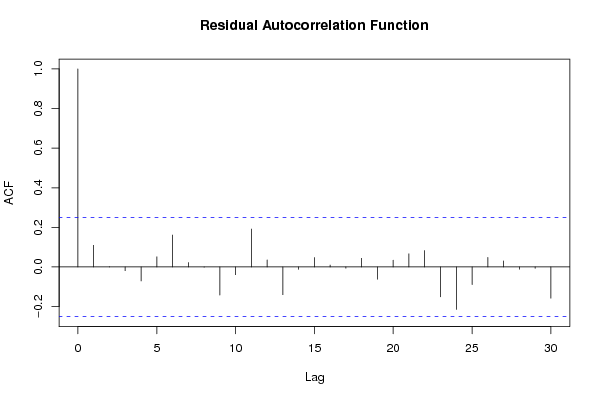

bitmap(file='test2.png')

acf(resid,length(resid)/2, main='Residual Autocorrelation Function')

dev.off()

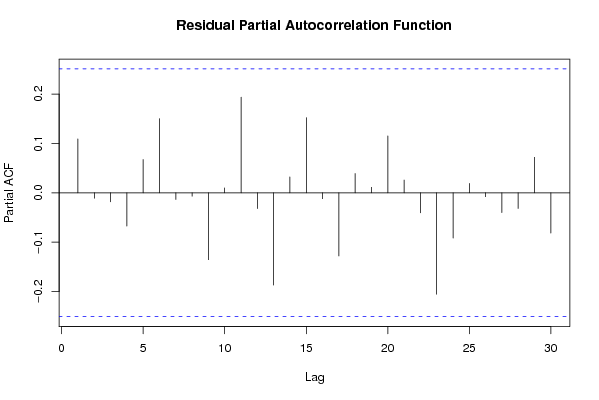

bitmap(file='test3.png')

pacf(resid,length(resid)/2, main='Residual Partial Autocorrelation Function')

dev.off()

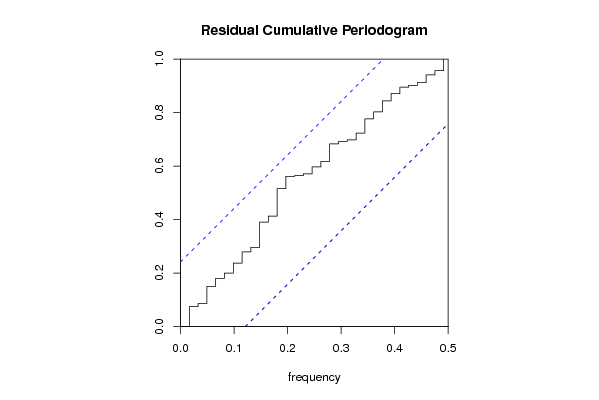

bitmap(file='test4.png')

cpgram(resid, main='Residual Cumulative Periodogram')

dev.off()

bitmap(file='test5.png')

hist(resid, main='Residual Histogram', xlab='values of Residuals')

dev.off()

bitmap(file='test6.png')

densityplot(~resid,col='black',main='Residual Density Plot', xlab='values of Residuals')

dev.off()

bitmap(file='test7.png')

qqnorm(resid, main='Residual Normal Q-Q Plot')

qqline(resid)

dev.off()

ncols <- length(selection[[1]][1,])

nrows <- length(selection[[2]][,1])-1

load(file='createtable')

a<-table.start()

a<-table.row.start(a)

a<-table.element(a,'ARIMA Parameter Estimation and Backward Selection', ncols+1,TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'Iteration', header=TRUE)

for (i in 1:ncols) {

a<-table.element(a,names(selection[[3]][[1]]$coef)[i],header=TRUE)

}

a<-table.row.end(a)

for (j in 1:nrows) {

a<-table.row.start(a)

mydum <- 'Estimates ('

mydum <- paste(mydum,j)

mydum <- paste(mydum,')')

a<-table.element(a,mydum, header=TRUE)

for (i in 1:ncols) {

a<-table.element(a,round(selection[[1]][j,i],4))

}

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'(p-val)', header=TRUE)

for (i in 1:ncols) {

mydum <- '('

mydum <- paste(mydum,round(selection[[2]][j,i],4),sep='')

mydum <- paste(mydum,')')

a<-table.element(a,mydum)

}

a<-table.row.end(a)

}

a<-table.end(a)

table.save(a,file='mytable.tab')

a<-table.start()

a<-table.row.start(a)

a<-table.element(a,'Estimated ARIMA Residuals', 1,TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'Value', 1,TRUE)

a<-table.row.end(a)

for (i in (par4*par5+par3):length(resid)) {

a<-table.row.start(a)

a<-table.element(a,resid[i])

a<-table.row.end(a)

}

a<-table.end(a)

table.save(a,file='mytable1.tab')

|